Uranium: 3 Companies, Three Approaches

Have to admit, I am a huge fan of nuclear power. Big reactors, small modular reactors, recommissioned old reactors, I like them all. So I was delighted to see The Oregon Group come out with a report entitled “The Great Uranium Disconnect”. You can and should download it, free, here.

The “disconnect” is really twofold. First, in the face of looming uranium supply shortages (well detailed in the Oregon Group Report) the spot price for uranium declined from over $100/lb in January 2024 to around $60 presently. The second disconnect is between the share prices of uranium producers, developers and explorers and that same looming supply shortage.

The Oregon Group Report goes into detail as to the geo-political, environmental, regulatory factors and actual use of uranium and how this affects both the spot and contract uranium markets. It’s complicated, but the basics of supply and demand suggest that the overall price of uranium is going up. Likely, way up.

Which is excellent news for companies like Canada’s Cameco (CCO.T). A savvy friend of mine suggested that the best way to make money in uranium is to buy Cameco and wait. Cameco produces uranium from mines in Saskachewan’s Athabasca Basin as well as mines in other jurisdictions. It is part of a joint venture which produces uranium in Kazakhstan, and it recently, in partnership with Mark Carney’s Brookfield Renewables, purchased reactor maker, Westinghouse Electric. If you want exposure to uranium and the nuclear industry at large plus a tiny dividend, Cameco is worth a look.

At a very different stage of development is NexGen (NXE.T). The company’s Rook 1 project, located in the Athabasca Basin, has a National Instrument 43-101 Measured and Indicated resource of 3754Kt grading 3.10% U308, containing 256M pounds of uranium. The project is scheduled for a hearing before the Canadian Nuclear Safety Commission in November, with further hearings in February 2026. Assuming approval, this is the last regulatory step before construction of the mine can commence.

NexGen is well financed, has a smart mining plan and is getting down to the engineering. Rook 1 will, almost certainly, become a mine. There are literally billions of dollars in measured and indicated to support its current 4.5 billion dollar market cap. Currently it is trading just under $8.00, down from its all-time high of over $12.00 back in November 2024. At the moment, the NXE share price seems to be a bit depressed by the current sag in the spot price of uranium.

NexGen is still exploring and drilling around the Rook 1 project. A few weeks ago, it reported the best drill hole it has ever hit.

Leigh Curyer, Chief Executive Officer, commented: “This intercept from RK-25-232 is geologically exceptional and represents a transformational moment taking PCE into a category to rival Arrow at the same stage of drilling. Discovering mineralization of this intensity so early in our 2025 program outpaces the success pattern experienced at the Arrow Deposit. Incredible, considering Arrow’s status on the world stage. To put this into context, the width of high-grade intense mineralization in RK-25-232 at PCE was first encountered at Arrow well into the delineation phase of resource definition. Together with Arrow, it’s validation a very significant regional mineralizing event has occurred at Rook I that we are only just beginning to assess the magnitude.

Given that the company is at least three, more likely five, years away from production, this might be a good entry point for patient money. Well worth a look.

What if you are impatient?

Saving the best for last. Wild Bill Sheriff rides again!

Several years ago, long before COVID, I was up in the Yukon at Golden Predator’s 3 Aces gold project. Zipping along in helicopters with Bill Sheriff leaning too far out, pointing to drill pads. I followed Bill down an exposed quartz vein to see visible gold in the ground. It was a ton of fun. Golden Predator sold the 3 Aces project to Seabridge and was, itself, later acquired by Sabre Gold. Bill and his wonderful wife, Janet, seemed to be done with gold.

The “what next” did not take long. Appropriately enough, Sheriff turned his attention to EnCore Energy (EU.V), which held a variety of gold and uranium prospective land in the US. EnCore also had an ongoing interest in Group 11 Technologies, originally conceived of as a vehicle for in situ precious metal extraction technology.1 However, its technological roots lay in in situ uranium extraction. The press release announcing the EnCore participation came out September 1, 2020.

Fast forward, past COVID, to December 2023 and EnCore’s year end shareholders’ letter. In three years, EnCore had advanced its drive towards uranium production and narrowed its focus to Sheriff’s home state of Texas. By January 2024, EnCore was able to provide a very positive update on its South Texas operations and on drill results from the land surrounding its Alta Mesa In-Situ Recovery (ISR) Uranium Central Processing Plant. Necessary permits and licences were all in place.

October 3, 2024, EnCore, with its joint venture partner, Boss Energy hosted the Grand Opening of its Alta Mesa In-Situ Recovery ("ISR") Uranium Central Processing Plant ("CPP") and Wellfield operation. Former President George W. Bush attended the festivities. EnCore was now in the exclusive club of US-based uranium producers.

Unlike many other uranium explorers and developers, EnCore is actually producing and selling uranium. It reported its financial and operating results for the first three months of 2025 on May 12, 2025. Not quite profitable yet, but you can see it from here.

EnCore’s shares traded at highs close to $7.00 back in May of 2024, now, with huge milestones passed and actually producing uranium, EnCore is trading around $2.40. The EnCore share price rather closely tracks the uranium spot price.

Two things are pluses for Encore: first, the haywire tariff antics of the Trump administration. Uranium imports from Kazakhstan face potential 27% tariffs, from Canada, 10%. Being based in Texas is a good thing. Second, EnCore is actually producing uranium from completed, paid-for, facilities. While it is, to a degree, at the mercy of the spot market, it also has the potential to ride that market back up.

The Oregon Group Report is very clear about one thing: demand for uranium will certainly go up, supply will too, but slowly. The spot market will gyrate, but its direction is pretty clear. Uranium is going to rise in price, perhaps dramatically.

(Disclaimer: I do not hold shares in any of the companies mentioned in this article. This is not investment advice. Do your own due diligence. Call the IR people for the big companies, call the CEO at EnCore.)

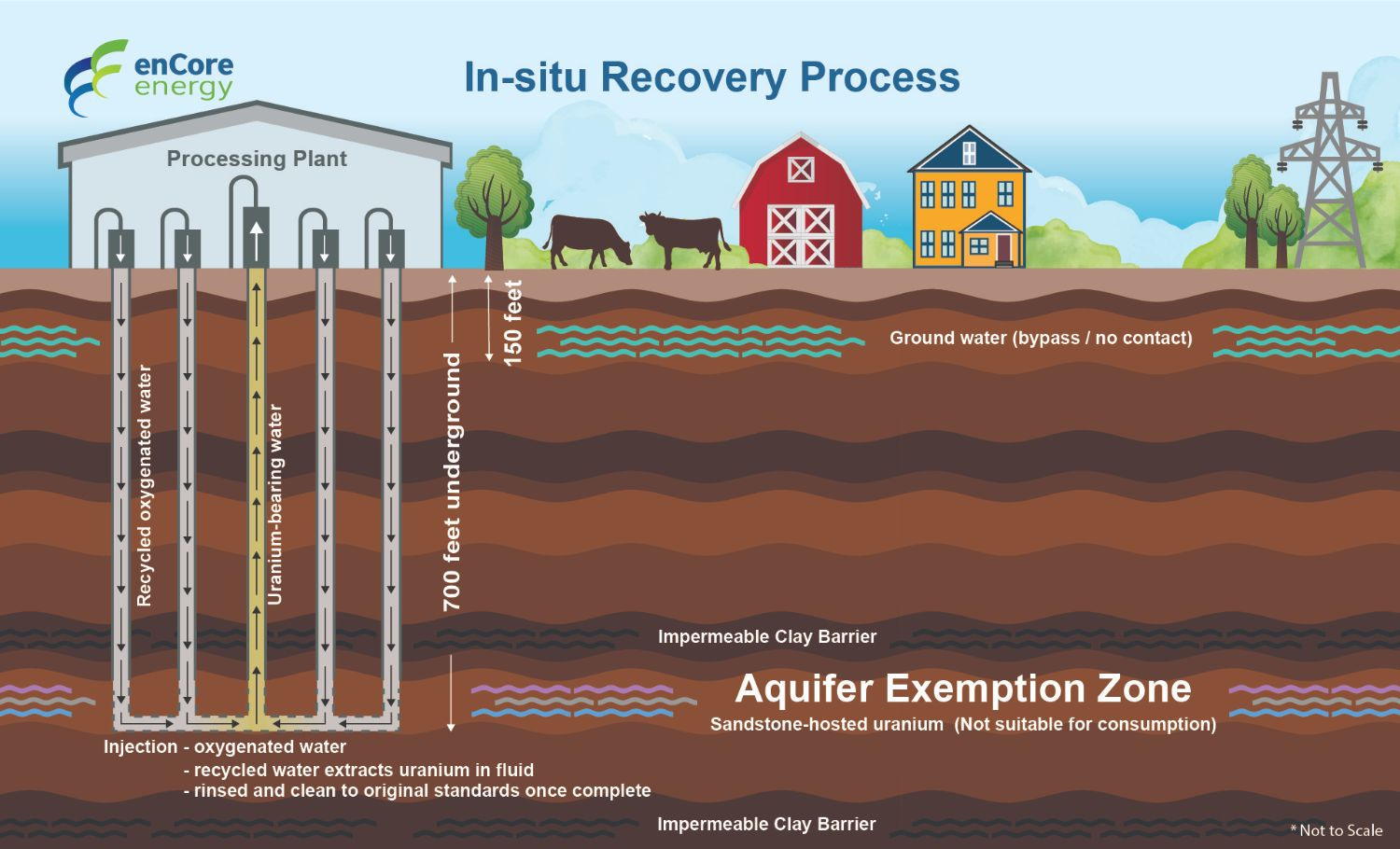

The diagram above is a very simplified version of the EnCore in situ recovery process. I’ll be in touch with Bill and Janet Sheriff and, a bit down the road, will do a substack on the details of the process. It is very clever, well tested and can, in the right conditions, see recoveries of 80% plus of the uranium available.