Unloved: Cartier Resources has Windfall Lake Surrounded

Gold is at $2500 USD/oz for the very first time. It looks like the beginning of a sustained rally. How high? No idea, and I am pretty sure it will drop back a little before taking off.

Very big news last Monday when Osisko Mining announced that it agreed to be taken over by Goldfields, its partner in the Windfall Project in Quebec. The transaction, valued at C$2.16 billion gives Osisko shareholders a 55% premium to the 20‐day volume weighted average trading price per Share. It gives Goldfields the remaining 50% of the Windfall project and a bit of a dog’s breakfast of other Osisko Mining assets.

The transaction refocuses attention on the highly prospective, gold producing, Abitibi greenstone belt. (A great map and historical summary of the Abitibi is over at the invaluable Visual Capitalist.) The key thing to understand about the Abitibi is that it has produced a lot of gold and will certainly produce more.

My own Abitibi “play” is Cartier Resources (ECR.V) and, like most other juniors, it is down from my initial purchase price. Down a lot. It recently traded as low as $0.04 which is both depressing and, in my view, a huge opportunity. ECR has five projects in the Abitibi with its flagship project, the Chimo Mine, a past gold producer.

I have written about Chimo before, here and here. The Chimo project has a PEA and an indicated and inferred gold resource of 2.3 million ounces. CEO Philippe Cloutier and his team have drilled near the 920 meter Chimo Mine main shaft (currently flooded but easily de-watered) and have now stepped out to drill the East Cadillac property looking for a new type of mineralization is found in sedimentary rocks where gold concentrations are, for this Project, generally higher than those found in volcanic rocks. As ever, adding ounces, especially high grade ounces, to an already attractive project increases the overall value of that project.

However, Cartier has three other projects which are closer to the Windfall project and likely to draw attention as the full implications of the Goldfields takeover become clear.

The Benoist Property is 55 kilometers to the west of Windfall. It has a small 43-101 Mineral Resource estimate compiled when gold prices were $1610 as opposed to the current over $2400 price. This is a property which needs more drilling and is an excellent joint venture prospect.

The Wilson Property hosts the Toussaint deposit which, on the basis of very preliminary drilling, is thought to contain 45,000 ounces of gold. An option on the Wilson Property, granted to Hawkmoon Resources, was recently terminated and Cartier’s 100% interest restored.

The Fenton Gold Project is to the north of Windfall. 325 meters long, 15-25 meters wide, Fenton has a non-43-101 historical estimate reports 426,173 tons grading 4.66 g/t Au corresponding to 63,885 oz Au of which 23,643 oz Au are located in the first 50 m below the surface based on 73 holes drilled on the three main areas of the Fenton Gold Deposit. Bringing Fenton into 43-101 compliance would require some additional drilling to confirm the earlier holes. However, it might make more sense to explore high chargability adjacent targets on the property in the hope of increasing the over all gold reserves.

Here’s the thing. If gold is actually in a big bull move it will take a while for the share prices of gold explorers to take off. First, producers, then development stories which are near production and then, well, people get excited.

2.3 million ounces of gold, a 900 meter shaft which needs dewatering but is intact, more ounces at Chimo to come. In itself, that is more than interesting. But the properties around the Windfall project will also create interest. A new junior wanting to jump into the “gold rush” could do much worse than to option an already prospected and historically drilled prospective gold property.

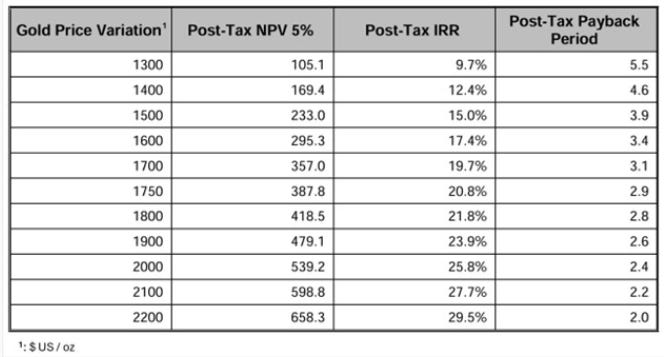

One other note: the 2023 PEA was done using a long term gold price of $1750 USD per ounce. It included a sensitivity table:

That table only goes to a gold price of $2200 USD. But the Post-Tax Payback period basically decreases by 0.2 years for every $100 rise in the price of gold. Which suggests that gold at $2500 leads to a Payback period of 1.4 years. Practically no time at all.

However, the PEA also projected that ECR would have to build a mill of its own which pushes the CAPEX up a lot (120 million dollars). However, there are several mills in the area with spare capacity. The PEA already has an ore sorter included in the CAPEX so ECR would be shipping high grade sorted rock and keeping trucking costs to a minimum. Now do the Post-Tax Internal Rate of Return (IRR) and payback period on a 180 million dollar CAPEX.

Put all this together with a $2500 gold price and the $21 million Cartier market cap seems extremely low. When the market swings round to gold explorers ECR will be at the front of the pack.

[Disclaimer: I own shares in Cartier Resources. I may buy or sell at any time. Do your own due diligence. Call the CEO.]