Marathon Gold: Nearly Mining in Newfoundland

Over at Motherlodetv.net, I followed Marathon Gold (MOZ.T) for years as it went from an interesting Newfoundland gold exploration play to a full blown development story. As happens, founding CEO Phil Walford moved on and new management wanted a different set of stories.

I last wrote at length about Marathon back in April 2019. Management changed and the shares marched upwards from a trading level around $0.80 to a high of over $3.40 in July of 2021. (I hope Phil held.) But from there, MOZ dropped like a stone and in this season of discontent is trading at $0.56.

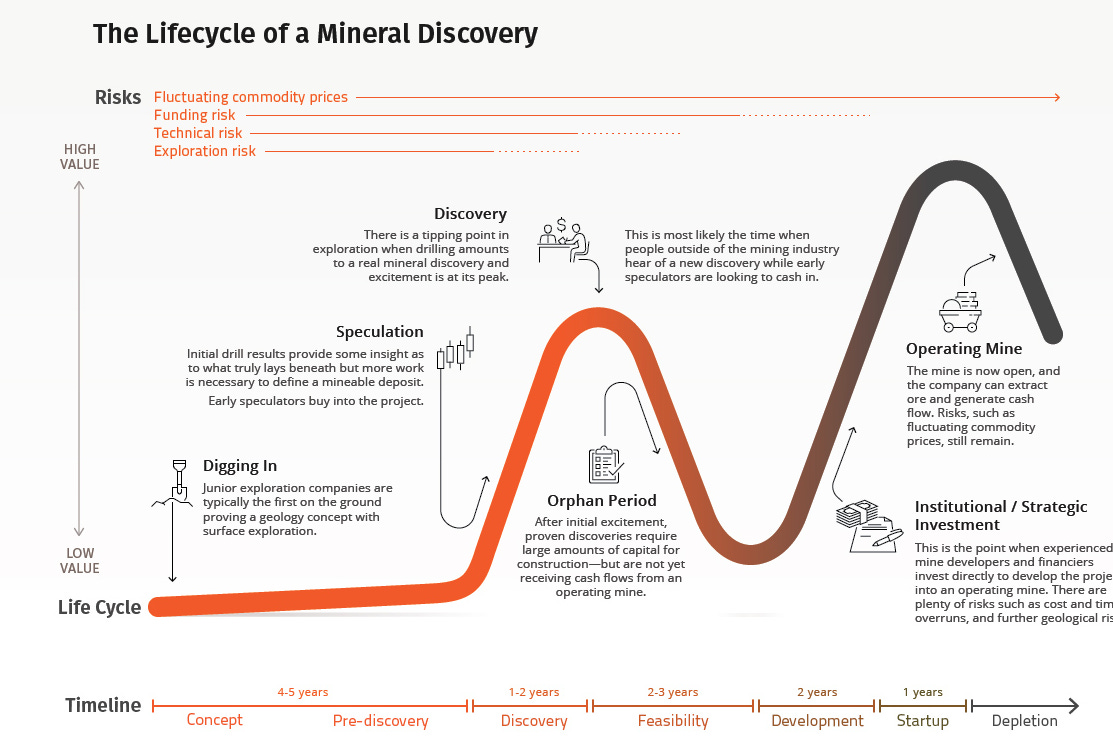

Welcome to the Lassonde Curve named after mining legend Pierre Lassonde who you can read about at the always informative VisualCapitalist.com where I stole this illustration:

If you take a look at the MOZ chart from 2018 to now it is pretty obvious that Marathon is in Lassonde’s “orphan” period which happens to coincide with the gold price going off and the junior market dragging along the bottom.

So, is MOZ a screaming buy at $0.56. Well, the consensus of analysts following the stock suggests it is: average target price in one year, $1.99 with a high of $3.50.

These are not unrealistic targets. Marathon has 4 million ounces of measured and indicated gold, another 1.1 million ounces inferred, a completed NI 43-101 Technical Report and Feasibility Study, is fully permitted and work has commenced on the actual mine at Valentine Lake.

Marathon was fortunate back in 2019 to link arms with Franco Nevada (FNV.T) when Franco Nevada acquired a 2% net smelter royalty for 18 million dollars. At the time, Phil Wolford was quoted as saying, “Franco-Nevada’s purchase of the NSR is a major endorsement of the Valentine Lake project by one of the best-known and regarded public royalty companies. The proceeds from this strategic financing transaction will allow Marathon to fast-track the completion of the Prefeasibility Study in early 2020.”

Which would have been great but COVID pushed back the completion date of the Pre-Feasibility. However, the study was completed in November 2022. Apparently, Franco Nevada liked what it saw and, in June 2023, took its Net Smelter Royalty to 3% for a payment of USD 45 million and did a bought deal on flow through shares for Canadian 6.9 million ensuring that MOZ’s continued exploration efforts were fully funded.

Which means that MOZ is well funded and likely to have sufficient money to reach its goal of gold production in Q1 2025. In its second quarter Management Discussion and Analysis (a must read item if you are looking at investing) the company states, “The Company’s cash balance of $130,205, and access to the US$225 million Credit Facility, leaves Marathon well positioned to execute on all its planned project construction and non-project construction activities for the remainder of 2023.”

Realistically, MOZ may need to do one more private placement prior to commencing mining in 2025. It would, of course, be better to do such a raise when the share price is a bit closer to the analyst’s targets. However, Marathon has made it this far issuing only 404,000,000 shares as of August 9, 2023. There are just over 88 million warrants and 16 million options outstanding but, it is not out of the question that MOZ could hit production with less than 600 million total shares outstanding even including a small raise.

In the current market, MOZ’s market cap is just over a depressed 225 million.

In its corporate presentation, updated September 2023, Marathon compares two other Canadian gold projects which have been bought out in the last 18 months: Great Bear, with 2.1 Moz and no permits bought by Kinross for 1.35 billion or $270 an ounce: Back River 6.3 Moz measured and indicated, permitted, located in Nunavut, bought by B2Gold for 1.1 billion or $120 an ounce measured and indicated. MOZ by comparison, has 4 Moz, is permitted and at the then 315 million market cap, is valuing the measured and indicated at $62 an ounce. (Now, about $45 an ounce at the current market cap.)

Probably the greatest challenge Marathon faces in capturing the full value of its assets is that the measured and indicated 4.0 Moz is considered to be a bit too small to attract a major’s bid. Which is why the ongoing exploration program could be very significant. On the one hand MOZ maybe able to bring a sizable portion of its 1.1 Moz inferred into the measured and indicated column. On the other, Marathon has a number of very prospective targets which are not included in its current Resource Estimate. 5 Moz is not at all out of reach.

So, I am looking at Marathon. Hard. It might be a little early. But, to be honest, I am not looking at playing for nickels here. If gold begins to recover and the junior markets can get off life support the analysts have every chance of being right. Which would be delightful.

[Disclaimer: This is not investment advice. I am not an investment professional. I am down about 30% at the moment. I will write about companies that I hold. I will disclose any holdings. Do your own due diligence. Do it hard. Call the CEO.

I currently do not hold shares in MOZ.T. A nibble. Rereading my article MOZ looks solid.]