Gold? What about Copper

Gold busts through $2900. Woot! I like gold, I love silver, but my bet is I’ll make money on copper.

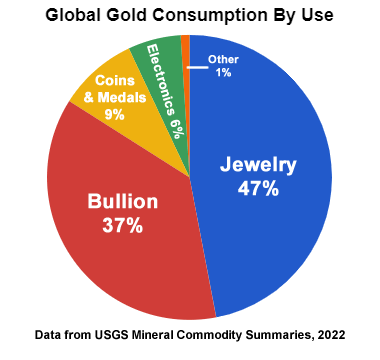

Gold is a great monetary metal. The ultimate store of value and so on. But the fact is that gold is also just a very rare, magic, rock. It has relatively few non-financial or jewellery uses. Here’s a chart from 2022 and I doubt much has changed.

Industry and dentistry account for about 7% of the gold used. The rest is in entirely discretionary uses. If gold disappeared tomorrow it would be a financial headache and a lot of Christmases and Indian holidays would be spoilt but the world’s industrial economy would be fine.

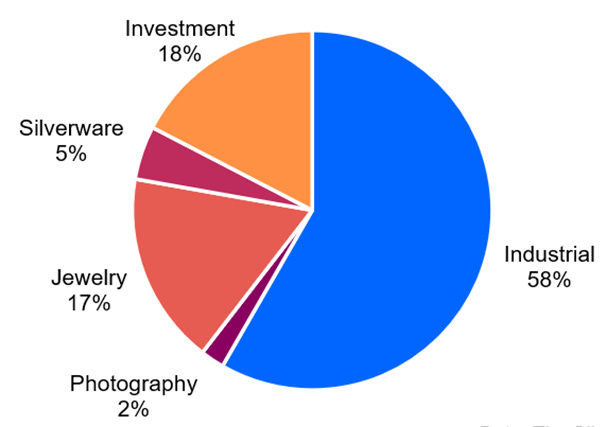

Silver is a different story. Here’s another chart from 2024:

As the silver bugs say, silver is an industrial metal and demand is growing as it is used extensively in solar panels and increasingly in military applications (fun fact: a Tomahawk cruise missile contains over 500 ounces of silver.) Sprott has a report which gives the details of silver use and its role in the “energy transition”. The silver bugs are not wrong.

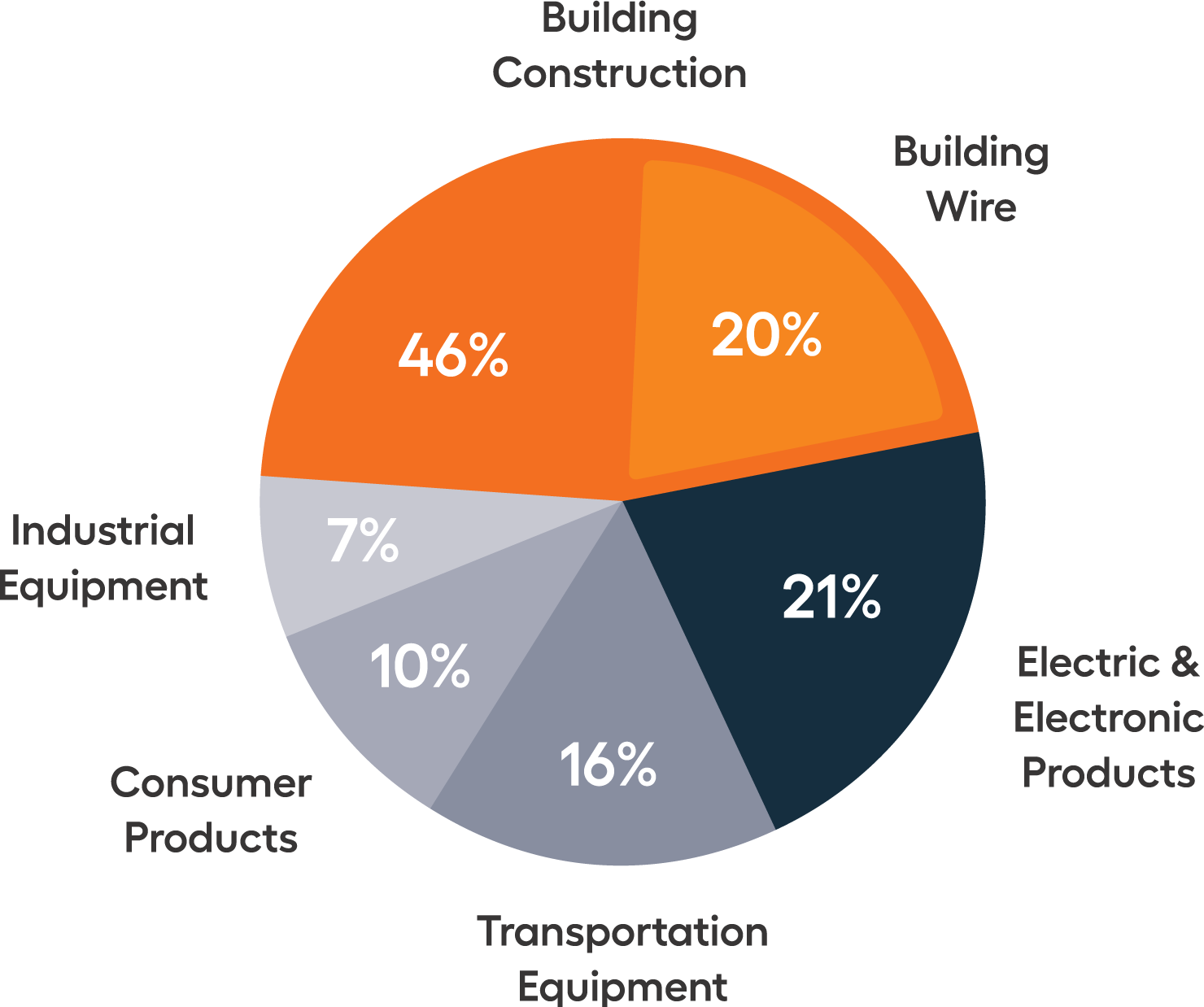

But silver is not an industrial metal like copper is. While there is a bit of copper held for investment purposes it does not even show up on copper uses charts such as this one from 2024:

The most interesting thing about copper from an investment perspective is that less of it is being mined than is being used: in 2022 there were 22MMT produced while demand was 26MMT. The shortfall was made up by drawing down reserves and recycling scrap copper. The price went up.

Investing in copper in 2020 would have been a smart move. But it may be an even smarter move now, especially in projects in the United States.

For whatever reason President Trump seems to love tariffs. (Personally, I think they are terrible economic policy, but I’m not the President.) He slapped (and tariffs are always “slapped”) a 25% percent tariff on all aluminium and steel coming into the United States. Last week he was asked if copper would be tariffed and he waffled a bit. As well he should as the US demand for copper is inelastic and its domestic capacity, while huge, is unable to meet it. Here is another chart from an excellent S&P Global study on Copper in the US:

You have to squint a bit but importing 767 thousand metric tons of refined copper is a lot. Putting a tariff on that would raise the price of refined copper without necessarily bringing on new supply. Amazingly, in the past, it has taken up to 29 years from discovery to final permitting for copper mines in the US.

I own shares in a number of copper or potentially copper-producing projects in both Canada and the US. Most are early stage exploration. Good IP or VTEM, drilling and figuring out the geology and the geometry.

My pal Graeme O’Neill is just waiting for assays on the first hole Bayhorse (BHS.V) is drilling from underground at the Bayhorse mine in Oregon. And across the Snake River, in Idaho, the Pegasus Project with two strong VTEM anomalies awaits. Copper porphyries. Maybe.

Down the Snake on the Idaho side at Mount Cuddy, Hercules Metals (BIG.V) is finishing up last years drilling assays. Robert Sinn of Goldfinger Capital is all over BIG and the privately held Scout Resources. It’s a long read but well worthwhile to understand what’s interesting enough to have Barrick, Teck, Rio Tinto and BHP all investing in a potential copper play. If you want a layman’s look at the potential of the Izee/Old Ferry suture belt you could do worse than reading my article from a little over a year ago, Hercules Silver: Is this close to Bayhorse?

The potential Izee Copper District is years away from producing copper or even having a company with a copper driven Mineral Resource Estimate. Intrepid Metals (INTR.V) is a good deal closer in Arizona. Close enough that Robert Friedland’s Ivanhoe Electric and Rio Tinto have staked claims adjacent on either side. This part of Arizona is peppered with copper deposits and INTR’s has the advantage of being quite near surface starting at ten meters. With good grades and a low strip ratio, INTR has to look attractive to its immediate neighbours and other, large, copper miners. Arizona is mining friendly.

My last American copper interest is in what a lot of people consider to be a mining unfriendly state: California. But US Copper (USCU.V) has pushed its Moonlight-Superior copper project forward to the PEA stage anyway. I wrote about the company a few weeks ago and the shares have not done much since. This is very much a joint venture/buy out situation. Which is only enhanced by the possibility of a Trump tariff on copper. Moonlight is very much a standing target for a company able to navigate the California permitting process. A process which is, in fact, navigable and getting more so by the day.

The Trump tariffs, as yet in abeyance for copper, make US copper assets all the more desirable. Well worth a look for investors with a year or two horizon and, maybe, a quick 10X if a major takes an interest.

(Disclaimer: I hold positions in BHS, BIG, INTR and USCU. I may buy or sell at any time. This is not investment advice. Do your own due diligence. Call the CEO.)

thanks for sharing, sir.