BIG and getting bigger

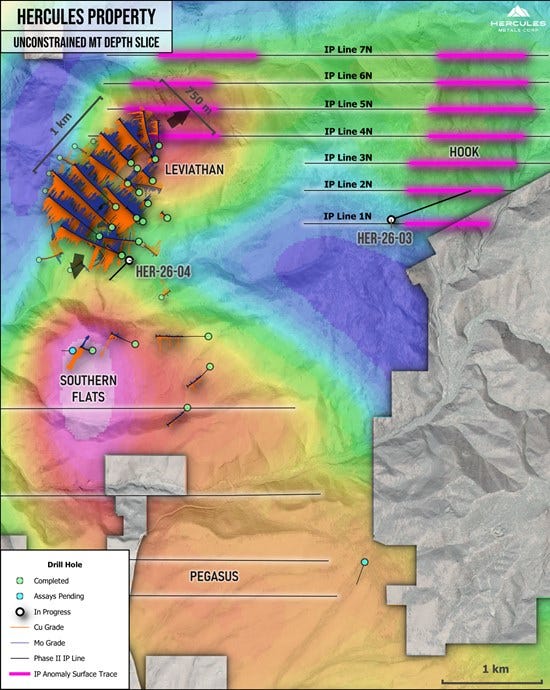

Just a quick update on Hercules Metals (BIG.V) which put out an interesting press release on July 2. The company was reporting the encouraging results of its IP survey of an area is is calling Hook. The IP suggests that there may be another copper porphyry to the south east of the original Leviathan discovery. More importantly, the IP indicates the anomaly begins only 100 meters from surface. The big knock against BIG is that while it may have found reasonable grades of copper, so far they have been 100s of meters below surface and therefore of marginal economic value. Drilling out the Hook anomaly has already commenced.

Oddly, while this release is certainly encouraging it is also troubling in that it suggests that the overall Hercules system is so large that it may be beyond the capabilities of a junior explorer to actually properly define. It takes nothing away from Chris Paul, CEO and his team, but right now they only have two drills turning on a project which is throwing off targets on the daily.

There are now four identified possible porphyries each of which could justify a three or four drill program in itself. My old mining buddy said it would take “100 million dollars and ten years” to fully define Hercules. Paul has already spent 60 million (more or less) and has more questions now than he did back in 2023. This is not a bad thing but getting answers to those questions will likely take much more than 100 million dollars. Think 500 million and likely more.

Right now BIG has 343 million shares out and a market cap of $209 million. Its shares are trading at $0.61. Where can Paul hope to find the money without dilluting current shareholders to essentially nothing? The private placement/LIFE route is not really suited to a long term, capital intensive, exploration program.

Normally, this would be the moment that a large balance sheet company would step up, thank Paul and his team for their efforts and say, “We’ll take it from here, lads.” The trouble is that Hercules with its multiple target zones is not really sufficiently advanced to be really attractive to a major. Again, this is to take nothing away from Paul or the project as a whole: it just reflects the misalignment of the junior resource model with really large projects.

I’ve written about the real problem faced by the dog who catches the car he is chasing - now what do you do? Paul and his team can continue drilling and hope that the Hook target has great grades close to surface and that the market re-rates BIG to a couple of bucks for the next round of financing. But that is not a plan, it’s a prayer.

A plan will likely include a strategic investment by a larger outfit willing to pay over market to gain a foothold in what is shaping up to be a major, American, copper play. Barrick was set to play that role a couple of years ago but, for whatever reason, stepped away.

BIG’s issue is not primarily geological. They have too much geology. No, the issue is how best to create shareholder value given that geology and the work left to be done to properly explore and define that geology.

As a shareholder in BIG I very much hope that the holes at Hook have great grades at fairly shallow depths and I will hold my shares until the results from this season are in. However, without a significant strategic partner coming on board, I will take profits as they arise.

(Disclaimer: I hold shares in Hercules Metals which I may sell at any time. This is not investment advice. Do your own due diligence. Call the CEO.)