Banyan Gold: Quietly rolling up the gold ounces

Under the radar, the perfect gold storm

People who know the Yukon have been, quietly, buying Banyan Gold (BYN.V) for years. It hit its all time high today at $0.51 and no one is very surprised.

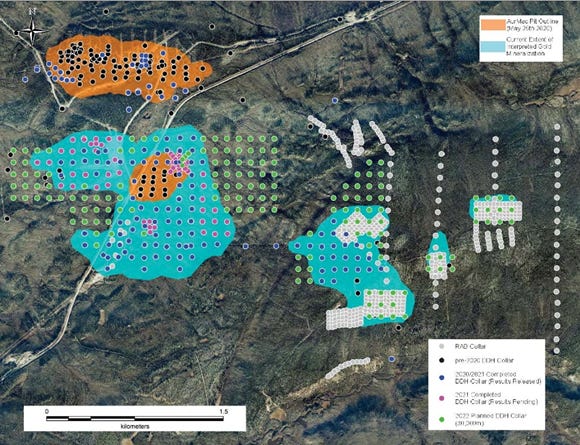

On May 17, 2022 Banyan released a revised 43-101 Resource Estimate for its AurMac Property located in the Mayo Mining district, approximately 56 kilometres northeast from Mayo, Yukon and 356 kms north of Whitehorse, Yukon.

4 million ounces of gold.

Near surface with many of the discoveries remaining open. This is very close to the Tier 1 Exploration target of 5 million plus ounces.

In the Resource Estimate press release, Tara Christie, Banyan’s CEO states, “This Resource Estimate demonstrates the value generated by Banyan with 40,000 metres of drilling adding over 3 million ounces of inferred mineral resources. All three deposits are open, with mineralization known to extend beyond the current block model boundaries.”

The 2022 drill program, planned to run 30,000 meters is almost certain to expand this gold resource.

An explorer within sight of 5 million ounces is big news. But Banyan has more than ounces in the ground. Frankly, I took my position long before the 4 million ounces seemed even possible.

I have visited the property - which in June is a mosquito-infested (and I mean infested) quasi-swamp. Tara and Paul Gray, Banyan’s wonderfully entertaining and dogged VP Exploration, did the “tour”. A few years ago, there was not much to see and we were all eager to escape the bugs. (I can see why Banyan is willing to drill in January in the Yukon where the temps drop to -40. No bugs.)

What AurMac consists of is a set of distinct, near-surface, low grade, high tonnage deposits. The sorts of rock which has made Victoria Gold (VGCX.T) the Yukon’s largest gold mine and one of Canada’s top producers.

Victoria Gold is one of the largest investors in Banyan and, in fact, along with Alexco (AXU.T), optioned the Aurmac properties to Banyan. Osisko Development (ODV.V) is another key investor.

Victoria Gold and Banyan Gold share the services of Paul Gray as their respective VP Exploration. Paul knows the territory and its geology and has been producing consistent results for both companies.

The great advantage that Banyan has is that a lot of the infrastructure, an all-weather road, dedicated electric power, and a fully operational mining/milling/leaching operation are down the road at Victoria’s Eagle mine.

As Christie said in her January Shareholders’ letter, “We only need to look down the road to Victoria Gold, to see a similar project – on and near-surface, low strip ratio, similar grade, heap leach mining operation – to have a comparable for our AurMac project. Victoria Gold’s ability to permit, build and operate the Eagle mine, demonstrates the viability of heap leach projects in Yukon and we can learn from their experiences on how to efficiently and successfully advance our heap leach projects. The economics of their recent build and actual operating costs will greatly assist Banyan when we start our Preliminary Economic Assessment (PEA) in fall of 2022.”

So, is AurMac Eagle II? I don’t think so. More like Eagle 2.1. Obviously, the terrain is different, but the rock seems similar. But what is very different is that Victoria was “flying blind” on all the issues Christie mentions in her letter. John McConnell, Victoria’s CEO, had no real precedent for a vast heap leach operation in the middle of nowhere. As Tara Christie acknowledges, Banyan can look down the road to see that operation in action.

My own investment in Banyan (and, dammit, I never had the money to invest in Victoria) is based on the belief that Banyan can go into profitable operation on a significantly accelerated timeline. Because there is a model down the road, everything from permitting to financing to actually designing the mine has the potential to be done more quickly.

Right now, Banyan has a market cap of $116,000,000 with a 43-101 resource of just under 4 million gold ounces ($29 an ounce). If Paul Gray remains true to form, the ounces in the ground will hit 5 million plus this year. The extra million ounces, at current valuation of $29 an ounce should add $29,000,000 to the market cap. Call it $0.13 a share.

But that is not what is likely to happen. The fact is that if Banyan can prove up 5 million ounces it will be “re-rated” as a Tier 1 explorer and will, I suspect, also move from explorer to developer.

It would not be a huge surprise to see Banyan teasing $1.00 by the end of 2022.

[Disclaimer: This is not investment advice. I am not an investment professional. I am down about 30% at the moment. I will write about companies that I hold. I will disclose any holdings. Do your own due diligence. Do it hard. Call the CEO.

I currently hold shares in BYN.V and while I have no plans to sell anytime soon, I reserve the right to take profits as they arise.]